Based on a quick look at the Edward M. Kennedy Institute for the United States Senate’s splash page, I wasn’t immediately sure what, precisely, the institute’s raison d’être might be. On the top menu bar there’s a slogan: “Just Vote.” Big clue?

On the About page, though, we are told its mission: “educating the public about the important role of the Senate in our government, encouraging participatory democracy, invigorating civil discourse, and inspiring the next generation of citizens and leaders to engage in the civic life of their communities.”

As for the vision thing, that’s supplied by its namesake, Ted “I Survived Chappaquiddick” Kennedy: “To preserve our vibrant democracy for future generations, I believe it is critical to have a place where citizens can go to learn first-hand about the Senate’s important role in our system of government.”

I guess that explains why the institute’s Boston location sports a replica room of the U.S. Senate chambers.

Which costs serious money, of course.

Paid for entirely by the ultra-rich Kennedys?

Fact check: no.

Some of it is paid for by you and me — courtesy of Congress and COVID!

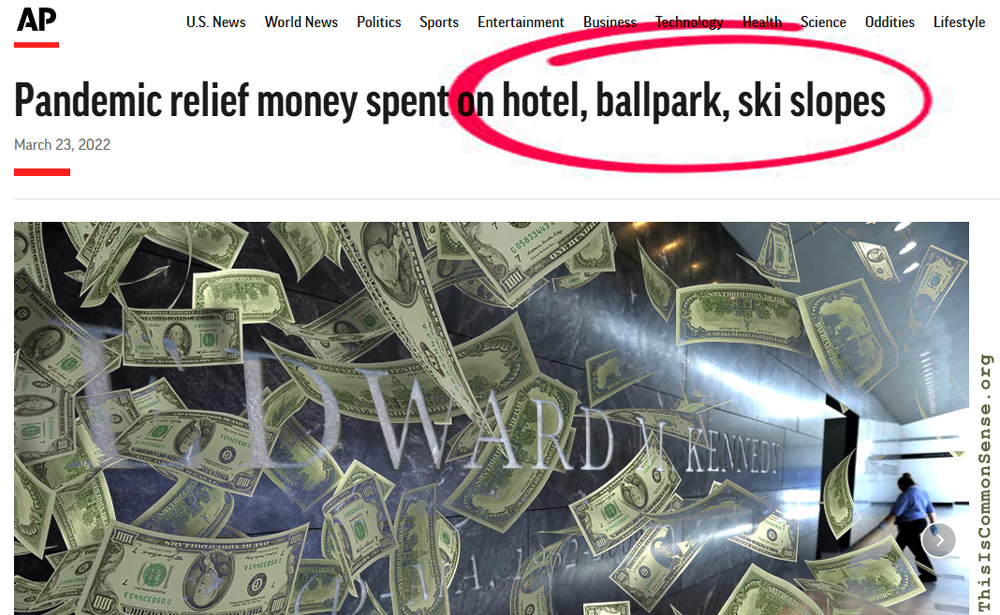

You see, part of last year’s $350 billion in pandemic relief went to Boston’s memorial outfit for its once-favored now-deceased multi-millionaire politician. Five million bucks, it turns out, was used (the AP tell us) to pay off the institute’s debt.

But don’t worry: the Kennedy Institute wasn’t singled out. Relief funds — which you might think would focus on struggling local libraries, community centers, and the like — also went to building a posh hotel and a minor league baseball stadium. And much, much more.

While politicians are good at spending money, especially for “emergencies,” they aren’t good at spending it well.

This is Common Sense. I’m Paul Jacob.

See all recent commentary

(simplified and organized)

See recent popular posts