Last week’s collapse of the Silicon Valley Bank gets more interesting with each revelation. But one of them is probably not that it was “woke.”

Contrary to rumor, I see no real evidence that SVB gave millions to Black Lives Matter. The bank did pledge $50 million towards an internal program dubbed “Access to Innovation.” This, we are told, “sought to connect women, Black people, and Latinos with startup funding, networking, and leadership development in the venture capitalist ecosystem.”

Sounds great in a press release, though what it has to do with making profits is a bit hard to determine.

Very feel-good, not very bottom-line.

And that’s where the bank failed, on the bottom line.

Its clientele was concentrated in one industry, which has been hit by rising interest rates. Thus stressed, it was exceptionally prone to “bank run” pressures. Its core asset class was long-term Treasury Bonds, whose value decreased with rising interest rates — and these were not hedged.

As Forbes put it, “Whether it was fully or semi-deliberate, Silicon Valley Bank was betting heavily on interest rates not rising.”

An extremely bad bet.

But you can see why the bankers would make it, right? Why wouldn’t they expect the giveaway mentality of Zero Interest Rates Forever?

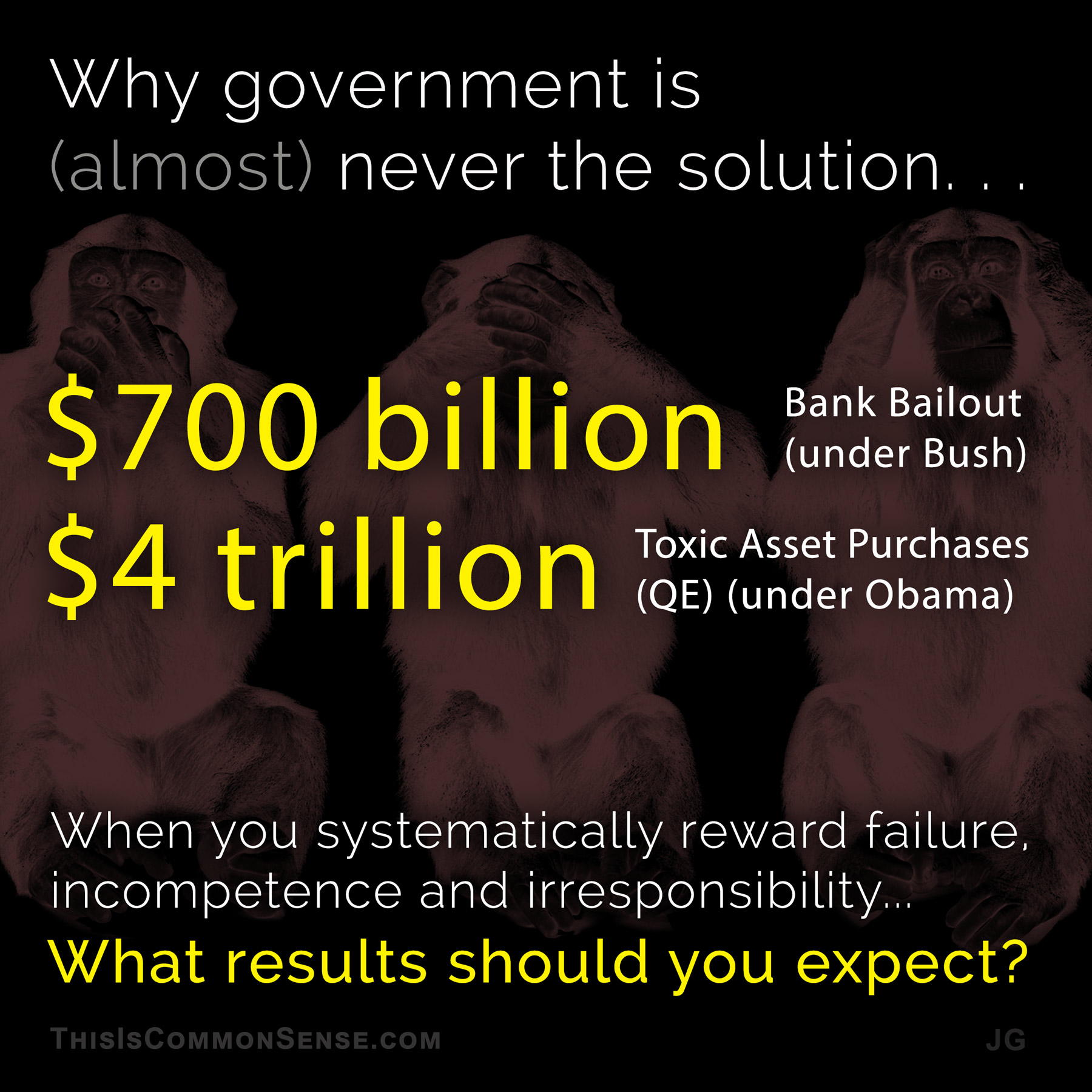

Their hopes dashed, they nevertheless turned to their friends . . . in power. The Biden Administration that failed to keep interest rates down then pledged to cover SVB’s clients — the super-rich corporations that true progressive Democrats pretend to hate for all their “profits” and “under-taxed” income — well above the FDIC-insured levels.*

We may learn real data about the banks’ wokeness levels, rather than mere rumor, but the bedrock truth reveals itself as all-too-familiar: it’s all about monetary policy.

That is, the “woke” ideas of a century ago, when the Progressives’ beloved Federal Reserve was created.

This is Common Sense. I’m Paul Jacob.

* Like Signature Bank, which was closed on Sunday, the overwhelming bulk of SVB’s deposits were uninsured by FDIC.

Illustration created with PicFinder.ai

See all recent commentary

(simplified and organized)

See recent popular posts