It’s a mess.

Families are often sold a bill of goods regarding higher education.

Unless a student pursues a subject like computer science, architecture, engineering, or medicine, it may take decades to pay off student loans.

Graduates who specialized in Advanced Basket Weaving, the Sociology of Postmodern Literary Stylings, and Marxist Techniques for Making White People Feel Guilty just might snag a high-paying job as an Ivy League professor or senior manager of a corporate “antiracism” task force. But beyond those few spots, opportunities are scant.

And, of course, many people who pursued legitimate studies in the liberal arts or technical subjects also don’t make enough to emerge from massive debt any decade soon. Nor does every STEM grad necessarily cash in. Individual results vary.

What to do?

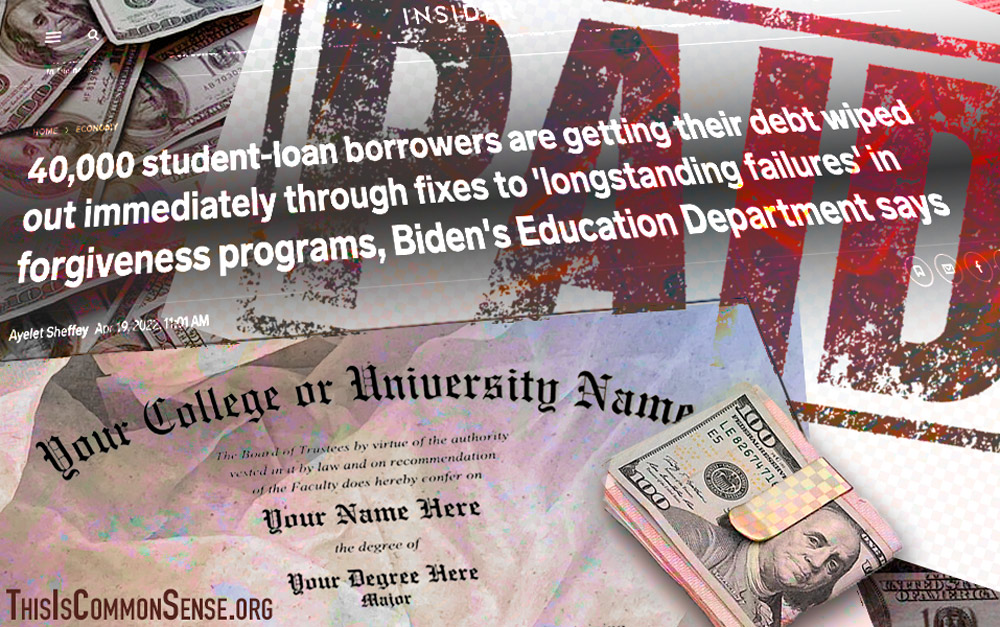

The Biden administration has decided to wipe out student debt en masse, expanding the Public Service Loan Forgiveness Program so that about 40,000 student-loan borrowers escape debt immediately and the debt of millions of others is slashed.

But is forcing others to pay this debt through their taxes — parents and children who perhaps carefully avoided taking out student loans — a just and practical answer to the problem?

The long-term solution is to get the government out of the business of subsidizing higher education in any manner, whether in the form of direct payments to schools or loans to students. Without the massive subsidies, tuition costs would decline.

The short-term solution? Launch an investigation into whether the U.S. Department of Education, colleges and universities — along with both Republican and Democratic administrations — have engaged in fraud against those who took out the loans.

If students were defrauded, first seek redress from the perpetrators. Not the taxpayers.

This is Common Sense. I’m Paul Jacob.

See all recent commentary

(simplified and organized)

See recent popular posts