The government should not be pushing private firms, including banks, to sever relationships with customers on ideological grounds.

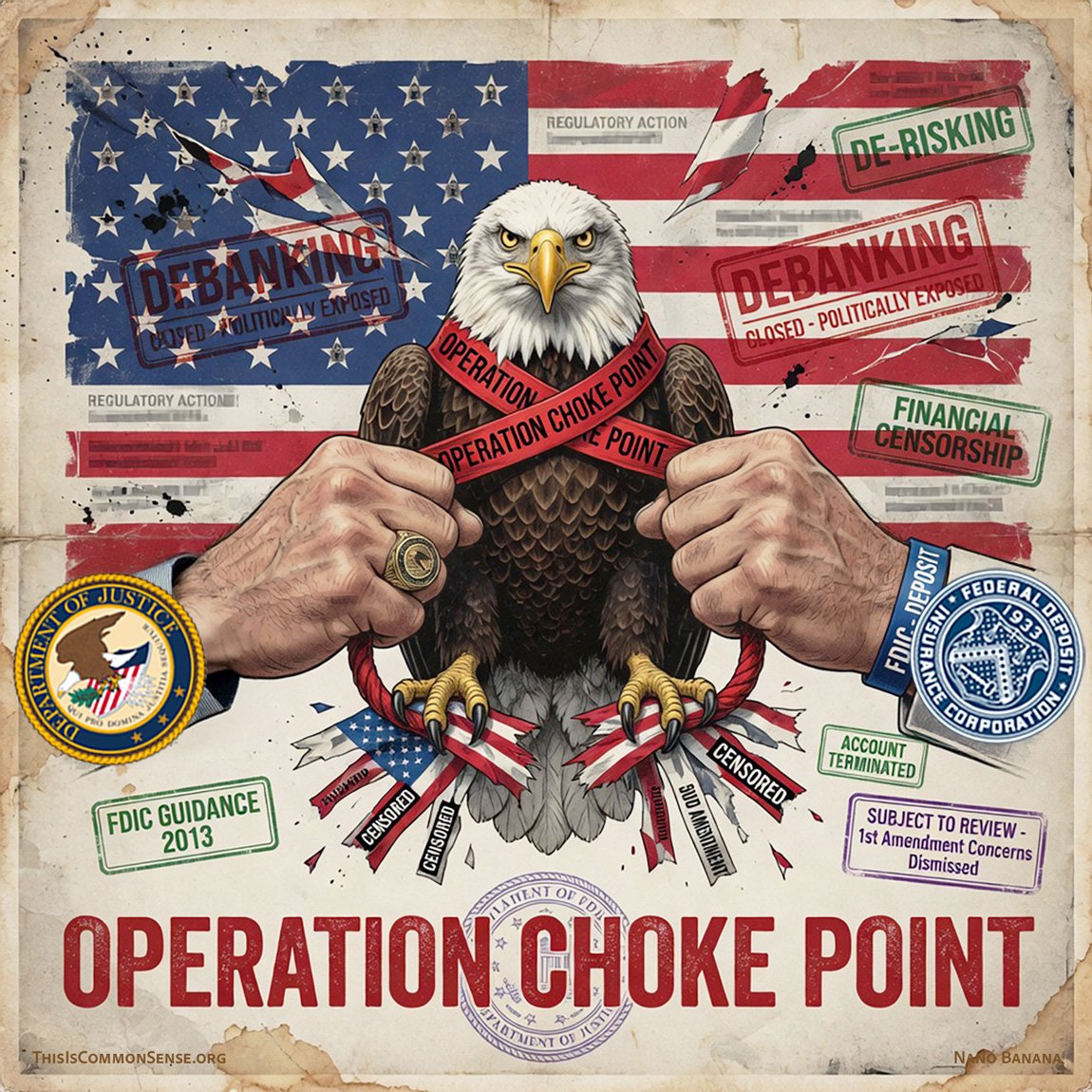

Nevertheless, in 2013 the Department of Justice and FDIC began pressing banks to cut off services to certain “high risk” industries, like the gun industry. The initiative was called — with laudable candor — Operation Choke Point. The pressure was an expression of the Obama administration’s hostility to Second Amendment rights and various views and advocacy, not a response to alleged lawbreaking by the debanked customers.

The Trump administration first sought to end this practice in 2017. But the urge to censor and punish viewpoints, including by debanking, resurged during the Biden administration.

In 2025, President Trump, in his second shot at heading the executive branch, issued a new executive order directing federal agencies to review the situation and issue new regulations to protect customers. It was to be made clear to banks that despite the impression conveyed by other administrations, so-called “reputational risk” — which boils down to hostility to certain views and enterprises — is not a warrant to fire customers.

A finalized and, one hopes, truly final rule has just been issued. It prohibits relevant agencies from criticizing or penalizing a supervised institution based on “reputation risk” or from instructing institutions to kill accounts because of customers’ constitutionally protected speech or activities.

The proper functions of government do not include acting to punish people directly or indirectly for their speech . . . or other exercise of their rights. The fact that just such a squarely improper (and illiberal) policy endured through several administrations shows just how shaky constitutionally guaranteed freedoms are in the current ideological climate.

This is Common Sense. I’m Paul Jacob.

Illustration created with Grok Imagine

See all recent commentary

(simplified and organized)

See recent popular posts

2 replies on “Operation Choke Point Choked”

In the absence of binding contract, the only “warrant to fire customers” any business should need is its desire to not to business with them.

Even if government agencies are prohibited from penalizing or pressuring institutions, such as banks, has the seed already been planted? Can the banks themselves, for example, take cues from government and media that certain customers should be denied access? Even if it goes against equal access laws, some organizations will succumb to the pressure of community activists. Freedom of association may still be endangered.